Global Broker Regulation Inquiry App

About WikiFX

English

简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

اردو

Volatile week for the markets. US inflation at highest level in 3 years. Gold falls below $4,100

Abstract:Key TakeawaysHigh U.S. CPI and PPI data boosted expectations of another Fed rate hike and pressured risk assets.U.S. stocks initially sold off on inflation and rate concerns before rebounding after Tr

Key Takeaways

High U.S. CPI and PPI data boosted expectations of another Fed rate hike and pressured risk assets.

U.S. stocks initially sold off on inflation and rate concerns before rebounding after Trump signaled progress toward a deal with Iran.

Rising Middle East tensions pushed oil prices higher, keeping inflation risks elevated globally.

Gold fell to multi-month lows as higher inflation and rate hike expectations increased Treasury yields.

The ECB raised interest rates, supporting the euro but adding pressure on European equity markets.

Technology and AI-related stocks remained volatile as investors questioned whether current valuations are sustainable.

The upcoming FOMC meeting is expected to be the most important market catalyst for stocks, gold, currencies, and cryptocurrencies next week.

US Inflation at Highest Level in 3 Years

The Consumer Price Index (CPI) in the US accelerated to 4.2% year-over-year, marking its highest level in three years, while Producer Price Index (PPI) data also showed persistent inflationary pressures throughout the economy. Higher energy prices, driven by tensions in the Middle East and disruptions around the Strait of Hormuz, played a significant role in pushing inflation higher.

As a result, investors significantly increased expectations that the Federal Reserve may need to keep interest rates elevated for longer and potentially deliver another rate hike before the end of the year. Market pricing now implies a growing probability of additional tightening, a sharp shift from expectations earlier this year that focused on rate cuts.

These developments put substantial pressure on gold prices, which fell below major support levels of $4,100 and reached their lowest levels since late 2025. Higher interest rate expectations increase the opportunity cost of holding non-yielding assets such as gold, leading investors to rotate into fixed-income assets offering higher yields.

U.S. Stocks Recovered From the Recent Selloff

Equity markets experienced a dramatic reversal during the week. The initial selloff was triggered by last weeks stronger-than-expected Nonfarm Payrolls report, which reinforced the view that the U.S. economy remains resilient despite higher interest rates. While strong employment data is generally positive for the economy, investors interpreted the report as reducing the likelihood of Federal Reserve rate cuts.

Technology stocks, particularly semiconductor and AI-related companies, came under pressure as higher interest rates threaten future growth valuations. The Dow Jones suffered one of its largest declines of the year, falling nearly 1,000 points during Wednesdays session, while the Nasdaq and S&P 500 also recorded sharp losses.

However, sentiment improved significantly on Thursday after President Donald Trump announced that planned military actions against Iran had been called off and suggested that negotiations were progressing toward a potential agreement. The announcement reduced fears of a broader regional conflict, helping equities rebound and improving overall market risk sentiment.

Investor rotation continued throughout the week, with money flowing out of technology and into defensive sectors such as healthcare, financials, and energy.

ECB Delivered 25 bps Rate Hike to Curb Inflation

The European Central Bank raised interest rates this week as policymakers continued their fight against persistent inflation across the Eurozone.

The decision initially supported the euro, with EURUSD moving higher as interest rate differentials between Europe and the United States narrowed. However, gains were limited as stronger U.S. inflation data simultaneously boosted expectations for a more hawkish Federal Reserve.

European equities reacted negatively to the ECBs decision, as higher borrowing costs increase pressure on economic growth and corporate earnings. Interest-rate-sensitive sectors such as real estate and consumer discretionary stocks faced the most pressure.

Oil Fluctuated, while Gold Remained Under Pressure

Escalating tensions between the United States and Iran pushed Brent crude above $93 per barrel and WTI crude above $90 per barrel as traders worried about potential disruptions to energy supplies passing through the Strait of Hormuz.

Although OPEC+ continues to gradually increase production, geopolitical risks remained the dominant driver of prices throughout the week.

Gold moved in the opposite direction. Despite traditionally benefiting from geopolitical uncertainty, the precious metal struggled as investors focused on rising inflation and higher interest rate expectations. Gold fell below key technical support levels of $4,100 and reached its lowest levels since November 2025.

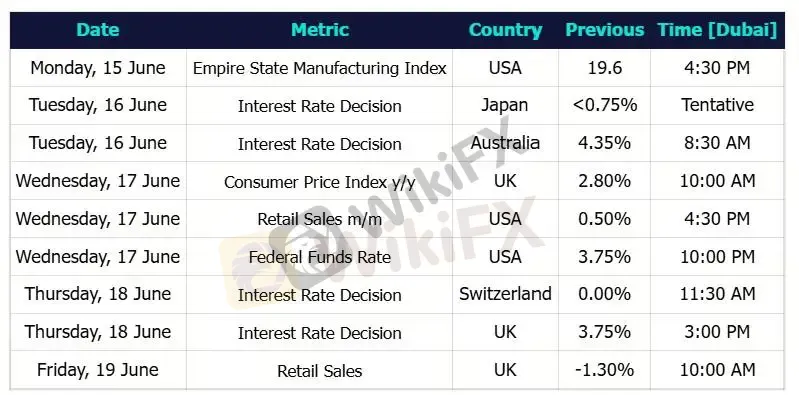

Major Economic Calendar Events for the Upcoming Week

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

TenX Prime Review: PAMM Blackout, Login Blocks, and Broker Regulation Questions

WikiFX

WikiFXInstaForex Review: Broker Profit Deductions, Login Shock, and Regulation Red Flags

WikiFXPosition Sizing Math For Steady Small Account Growth

WikiFXOcta Review 2026: Severe Withdrawal Complaints and Regulation Warnings

WikiFXUniglobe Markets Review 2026: Should You Trade with This Broker?

WikiFXWorld Cup · Forex Predict & Win Event

WikiFXZenstox Review 2026: Unexplained Profit Cancellation & Account Termination Allegations

WikiFXECB hikes interest rates for first time since 2023 as Iran war ramps up energy costs

WikiFXRaiseFX Review 2026: Is This Forex Broker Safe?

WikiFXIBKR VIP limited Review: No Regulation, Withdrawal Blocks, and a Broker Warning

WikiFXCurrency Calculator

USD

CNY

Current Rate:0

Enter amount

USD

Redeemable Amount

CNY

Calculate