Broker Globale Piattaforma di Verifica Regolamentare

WikiFX

Italiano

简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

اردو

ETO Markets TrendWatch: U.S. Private Credit Stress Breaks into Full Crisis

Sommario:In March 2026, the U.S. private credit market entered a phase of catastrophic deleveraging.Software‑heavy portfolios, in some cases exceeding 50 percent exposure, came under pressure as refinancing st

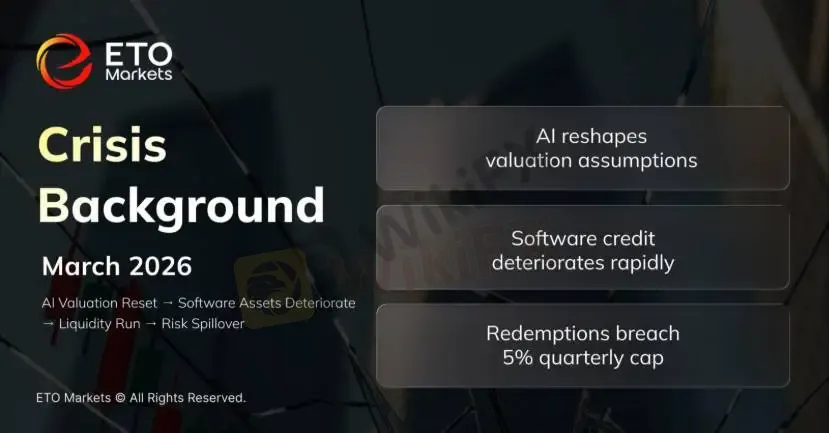

In March 2026, the U.S. private credit market entered a phase of catastrophic deleveraging.

Software‑heavy portfolios, in some cases exceeding 50 percent exposure, came under pressure as refinancing stress and a forward‑shifted maturity wall drove rapid asset‑quality deterioration and liquidity strain.

ETO Markets highlights how declining asset quality triggered a surge in redemptions and subsequently transmitted pressure to banks and broader credit markets through interconnected exposures.

AI Repricing: Software Credit Quality Hit First

The initial shock stemmed from a reassessment of credit quality in the software sector.

AI disruption has weakened the industrys business models, pricing power, and cash‑flow stability. Morgan Stanley warned that default rates in direct lending could climb to 8 percent, the highest level since the pandemic.

The maturity wall has also shifted forward. PitchBook data shows that 11 percent of software‑related direct loans mature in 2027 and another 20 percent in 2028. Highly leveraged borrowers are being forced into early credit cleansing under technological pressure.

Liquidity Shock: Secondary‑Market Discounts Deepen Losses

Liquidity stress surfaced as assets were repriced.

In late February, Blue Owl Capital was forced to sell loan assets at steep discounts to meet redemption demands, triggering a sharp deterioration in market sentiment. Private credit, traditionally viewed as a hold‑to‑maturity and low‑volatility asset class, was abruptly transformed into a traded asset under liquidity duress, pushing price anchors sharply lower. The episode was widely interpreted as the private credit markets margin‑call moment.

Contagion quickly spread to larger institutions. BlackRock wrote down a USD 25 million loan to zero and imposed a 5 percent redemption cap on its USD 26 billion private credit fund, even as investor redemption requests approached twice that limit.

The shift from discounted sales to rapid write‑downs signaled a transition from valuation skepticism to concerns about actual realizability. Pricing became dominated by liquidity premia rather than fundamentals.

Redemption Pressure: Funds Move to Active Gating

The liquidity crunch forced asset managers to tighten redemption mechanisms across the industry.

· Cliffwater: Faced 14 percent redemption requests and capped quarterly payouts at 7 percent.

· Morgan Stanley: Capped withdrawals at 5 percent for its USD 8 billion North Haven Private Income Fund.

· Blackstone (BCRED):Fulfilled 7.9 percent redemptions supported by internal capital rather than improved liquidity.

Across the USD 1.8 trillion U.S. private credit market, redemption demand now exceeds the structural 5 percent quarterly limit across the market, pushing the industry from passive deleveraging to active liquidity control.

Systemic Spillover: Shadow Banking Hits Traditional Banks

Through complex credit linkages, risks have migrated into the real economy and the regulated banking system.

· Deutsche Bank disclosed EUR 25.9 billion in private‑credit‑related exposure, representing about 5 percent of its loan book.

· FDIC data shows that by the end of 2025, U.S. banks had USD 1.4 trillion in loans to non‑deposit financial institutions, with an additional USD 2.8 trillion in undrawn commitments.

This implies potential exposure of USD 4.2 trillion if private credit funds draw down their credit lines simultaneously.

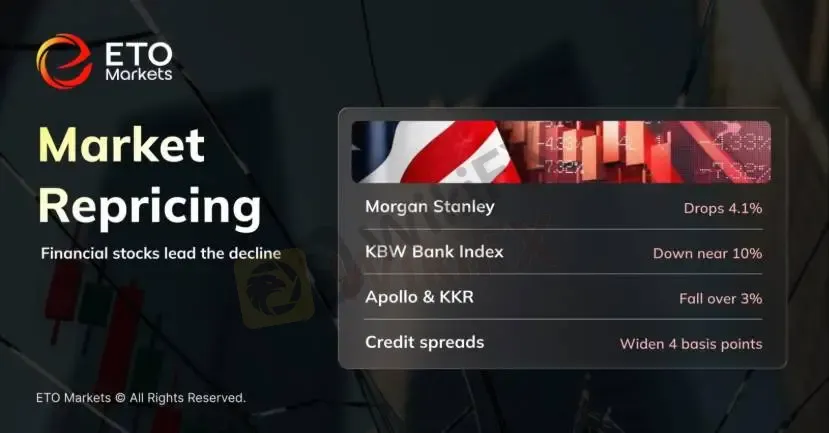

Market Reaction: Financials Lead the Sell‑Off

Since mid‑March, financial stocks have been hit hardest as systemic risk expectations rise.

· Morgan Stanley fell 4.1% in a single session.

· Apollo, KKR, and Ares all dropped by over 3%.

· The KBW Bank Index has retreated nearly 10% YTD, significantly underperforming the S&P 500.

· Investment Grade (IG) credit spreads widened by 4 bps in a single week, the largest move in months.

Markets no longer view private credit stress as isolated. Instead, they are repricing risk across banks, alternative asset managers, and the broader credit complex.

Disclaimer

The information contained herein is for general reference only and does not constitute investment advice, a solicitation, or an offer to buy or sell any financial products.

ETO Markets does not guarantee the accuracy, completeness, or timeliness of the information and shall not be liable for any losses incurred from reliance on such content.

Disclaimer:

Le opinioni di questo articolo rappresentano solo le opinioni personali dell’autore e non costituiscono consulenza in materia di investimenti per questa piattaforma. La piattaforma non garantisce l’accuratezza, la completezza e la tempestività delle informazioni relative all’articolo, né è responsabile delle perdite causate dall’uso o dall’affidamento delle informazioni relative all’articolo.

WikiFX Trader

vantage

Sotto supervisione

FxPro

Sotto supervisione

FXCM

Sotto supervisione

EBC FINANCIAL GROUP

Sotto supervisione

HFM

Sotto supervisione

AVATRADE

Sotto supervisione

vantage

Sotto supervisione

FxPro

Sotto supervisione

FXCM

Sotto supervisione

EBC FINANCIAL GROUP

Sotto supervisione

HFM

Sotto supervisione

AVATRADE

Sotto supervisione

WikiFX Trader

vantage

Sotto supervisione

FxPro

Sotto supervisione

FXCM

Sotto supervisione

EBC FINANCIAL GROUP

Sotto supervisione

HFM

Sotto supervisione

AVATRADE

Sotto supervisione

vantage

Sotto supervisione

FxPro

Sotto supervisione

FXCM

Sotto supervisione

EBC FINANCIAL GROUP

Sotto supervisione

HFM

Sotto supervisione

AVATRADE

Sotto supervisione

Rate Calc

USD

CNY

Tasso di cambio attuale:0

inserisci l'importo

USD

A disposizione

CNY

Calcolare