If the economy is good, why do so many big American companies look so unstable? - Business Insider

Abstract:OPINION: Half of corporate investment-grade bonds are one notch above junk, and a lack of investment in productivity could be to blame.

Even though a bunch of US economic indicators are looking good and interest rates are low, half of investment-grade corporate bonds are just one notch above junk status.This could be because levered US corporates have used their debt in ways that aren't productive for the economy and don't contribute to corporate profitability.That means that as the economy shows signs of slowing, weak hands could have a harder time servicing their debt.This is an opinion column. The thoughts expressed are those of the author.Visit Business Insider's homepage for more stories.

“Our economy is the best it's ever been,” President Donald Trump said while touting his administration's policies during his State of the Union speech this week.He cited a rising stock market, low unemployment numbers, and rising wages — which have yet to compare to precrisis boom times but are still inching up — all as reasons to rejoice.And indeed, consumer confidence, as measured by The Conference Board, increased to 131.6 in January from 126.5 in December. It was the survey's highest reading since August.Unfortunately, this message of prosperity has clearly not reached America's corporate-bond market.There, in the space where companies trade their debt, it appears conditions are deteriorating. As Scott Minerd, the global chief investment officer of Guggenheim Investments, said at the World Economic Forum last month, 50% of the investment-grade corporate bond market is rated BBB by credit-rating agencies, a notch above the level where debt is considered “junk bonds” (or as we now say politely on Wall Street, “speculative grade”). In 2007 that number was 35%.

That so many companies are teetering on the edge worries Minerd, to say the least.“We expect 15% to 20% of BBBs to get downgraded to high yield in the next downgrade wave: This would equate to $500 [billion] to $660 billion and be the largest fallen angel volume on record — and would also swamp the high-yield market,” he said. “Ultimately, we will reach a tipping point when investors will awaken to the rising tide of defaults and downgrades. The timing is hard to predict, but this reminds me a lot of the lead-up to the 2001 and 2002 recession.”But why worry, Minerd? Yes, corporate debt is high — nearing $10 trillion and pushing the US to a record 47% debt-GDP ratio — but interest rates are low and don't appear to be going up anytime soon. Plus, corporations have cash. Under these economic conditions, you could argue that corporations in need could just refinance their debt and be fine. It's why some say that bond bears are overstating the risk here.It's what you do with itBut there are two problems with this way of thinking. One is, of course, that rosy financial conditions will not continue forever. The other is that, as the folks over at the International Monetary Fund wrote in their “Global Financial Stability Report” last fall, corporate debt “has risen and is increasingly used for financial risk-taking — to fund corporate payouts to investors, as well as mergers and acquisitions (M&A), especially in the United States.”

Put another way, it isn't just that this debt exists; it's that it's being used in ways that aren't particularly productive for the overall economy. Balance sheets are getting loaded up, but companies don't have much to show for it aside from soaring stock prices.Despite the magnanimity of Trump's corporate tax cut, starting last year business investment has been in its longest slump since 2009. Instead of using cash to invest in things that would make the economy and their companies more productive — like new equipment, better-trained or paid workers, or research and development — corporate America just paid out its shareholders and itself.In 2018, “the S&P 500 Index did a combined $806 billion in buybacks, about $200 billion more than the previous record set in 2007,” according to the Harvard Business Review. Goldman Sachs called corporate buybacks “the most dominant source” of demand for stocks last year, while warning that purchases were beginning to wane.Say what you want about buybacks, but they don't make the economy or a company more productive. They don't pave the way to higher corporate profits. Neither do dividends to shareholders. And it seems this lack of investment is starting to show in our economy. In the third quarter of last year, productivity fell for the first time since 2015. It is a trend that some economists, such as Ian Sheperdson, the chief economist at Pantheon Macroeconomics, say is likely to stay with us for a bit.“The year-over-year rate of growth of real business capex has slowed from a recent peak of 6.9%, in Q2 2018, to just 0.3% in the fourth quarter of last year,” he wrote in a recent note to clients.

“A dip below zero, for the first time in five years, looks almost inevitable in the first quarter, thanks to the combination of adverse base effects and a near-flat trend in the quarterly run rate. Against that backdrop, we are confident that productivity growth will slow this year, to about 1%. The fourth quarter increase was probably about 1.6% annualized, but that's just not sustainable as businesses pull back their spending.”A dangerous cocktailNow, combine high debt levels with a misallocation of capital and the fact that corporate profits have been falling for the last two quarters. Sure stocks are ripping, but according to FactSet companies in the S&P 500 are projected to report a 2% decline in fourth quarter earnings from the same time in 2018. That is why Goldman Sachs said stock buybacks are about to ebb too.

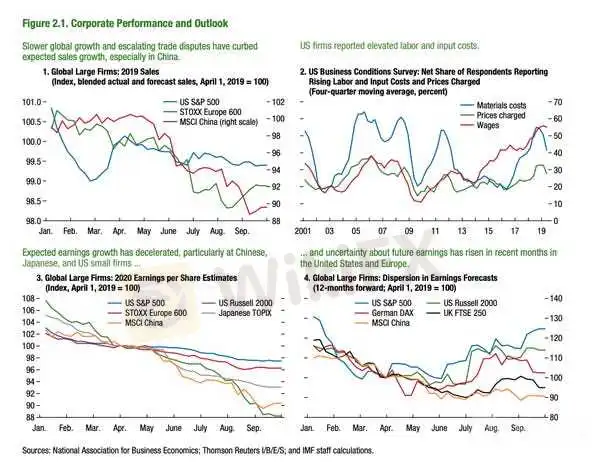

IMF Global Financial Stability Report

For companies on the brink of junk (I'm sorry, “speculative grade”) status high debt, low productivity and lower profits are a dangerous cocktail. Taken all together it could make debt servicing more challenging for companies in rough shape.For investors it's a cocktail made all the more dangerous by the fact that corporate credit spreads have been so tight, lulling them into a false sense of security as they chase higher yields.

“Ultimately, this leads to what he called a Ponzi Market where the only reason investors keep adding to risk is the fear that prices will be higher tomorrow (or in the case of bonds, yields will be lower tomorrow),” Minerd said in Davos.So why are so many companies teetering on the edge of junk status in a relatively healthy economy? Consider this: The word credit comes from the Latin word for trust, and what the corporate bond market may be telling us is that it can no longer trust in corporate America's ability to invest productively, hurting profit generation. It may be telling us that even in a world of extra low interest rates eventually debt — and what you do with it — matters.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

Read more

EBC Research Institute Hotspot Analysis | China Unleashes Major Moves, Stock Market Brews a Violent Reversal

The Chinese government has taken measures to boost the stock market, yet the market still faces challenges, and investors should proceed with caution.

How does the Stock Market Volatility Impact Forex Trading?

While the Stock market and the Forex market are two of the most significant components of the global financial system, interestingly, both are closely interconnected. It is no secret that stock market volatility can affect various aspects of the economy, but how does it affect Forex trading? Join us on this journey to learn how volatility in the stock market affects Forex trading and what forex traders can do to mitigate risks and seize opportunities!

How does the Stock Market Volatility Impact Forex Trading?

While the Stock market and the Forex market are two of the most significant components of the global financial system, interestingly, both are closely interconnected. It is no secret that stock market volatility can affect various aspects of the economy, but how does it affect Forex trading? Join us on this journey to learn how volatility in the stock market affects Forex trading and what forex traders can do to mitigate risks and seize opportunities!

Asian Stock Market Updates

Asian stocks extend global rally to 7th day, U.S. stimulus in focus.

WikiFX Broker

Latest News

DESPITE A SHARP FALL IN FX, FOOD COSTS CONTINUE TO RISE.

Complaint against Capitalix

Binance Elevates Dubai's Crypto Status with Full VASP License

eToro Added 509 Fresh Stocks and ETFs

MetroTrade Now NFA Member & CFTC Introducing Broker

Alert: Beware Of Unlicensed Scam Trading Broker ProMarkets

As Soaring Gold Prices Spark Enthusiasm,WikiFX Helps You Avoid Illegal Platforms’ Traps

Investor Scammed as Orfinex Withholds Funds and Negligently Trades Accounts

Hedge Funds Boost Gold Investments Amid Inflation Surge

EXPERT-OPTIONTRADE IS A RED FLAG

Currency Calculator